|

Apr 20 2011:

COMPARING YUM BRANDS and MCDONALDS

After hours, the

earnings came out on YUM. They are up 7% or .63 cents a

share before a special one time cost which reduces the

earnings to .54. YUM's earnings continue to get good but

here is why I prefer my strategy over owning any shares. I

am sure earnings like those today will jump the stock higher

for a while and might even set a new higher trading range,

but overall I prefer to be on the cautious side. The

earnings for the past 5 quarters are below. As long as the

earnings can stay above last year, then YUM will trade

higher or at least in a higher range, but earnings from the

US were down. Overall just 1%, but it shows the weakness of

the world's biggest economy. In the US not only is there

more competition, but the cost of food is being reflected in

the declining US dollar. Meanwhile earnings outside the US

and in particular Asia are very good, up 18% in China and 5%

worldwide. This is excellent news, but lets look first at

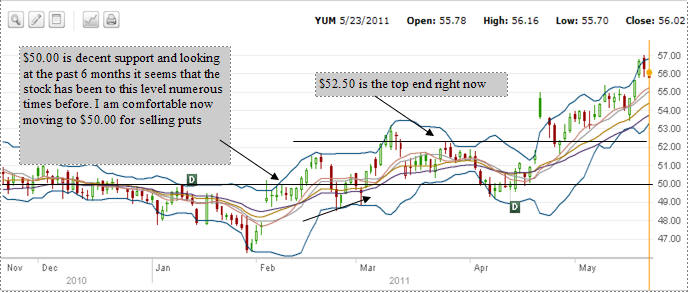

the chart below. Since March's earnings YUM stayed sideway

until September when YUM turned in a stellar performance and

the forward looking statement promised more growth. The Dec

earnings of .63 cents was good but not quite what a lot of

investors believed after September's earnings. The stock

pulled back from Dec through to Feb and despite the market

itself moving higher into Feb 2011, YUM moved to a low on

Feb 24 of $48.67. But while the earnings were good after

hours, overall the earnings of .63 cents matches December's.

The lower Bollinger is my key to when this stock may set a

new trend. I have set my trading range between the upper

Bollinger from the previous range and the lower Bollinger

from the most recent move, around the $48 strike.

Once the lower Bollinger holds

for a few months and can confirm a move to a higher trading

range then I will move up, but until then every move to the

lower Bollinger should give me the opportunity to sell more

naked puts within my range.

Meanwhile here is how I view

both YUM and the other large restaurant stock, McDonalds.

Now here is a comparison chart

of both companies. The larger gain in YUM is evident plus

YUM has set two new higher highs. Meanwhile McDonalds has

failed to set a new high since December of 2010. This is the

reason for the larger return on equity and return on

investment for YUM. Meanwhile though McDonalds has a better

dividend, much better debt to capital ratio, lower PE,

better earnings, cash flow and of particular interest book

value. However the market cap is much larger for McDonalds

but revenue is much better at YUM. The two charts below show

that both have decent trading ranges. I find both stocks are

excellent for selling naked puts. Earnings continue to

support a decent trading range for both stocks particularly

watching the lower bollinger.

SUMMARY:

Both YUM

and McDonalds have been excellent stocks for my portfolio.

Recent earnings from YUM show good growth outside the US,

and while analysts talk up the stock, I tend to look at it

more for its range. At .63 cents the recent quarter matches

December and does beat last year's same quarter. However

could the stock be ahead of itself? The PE is higher on YUM

than McDonalds, debt is larger, book value less, but on the

other hand YUM has provided a better return on equity and

investment for shareholders and has set two new highs since

Nov 2010. I always take a different approach to stocks and

both of these are good examples. For my strategy of selling

naked puts I am seeking stability of price and a

trading range rather than being concerned about the stock

climbing higher. In fact, a higher priced stock often

increases the risk of the stock pulling back in any selling

and could catch my naked puts and put me in the money.

Unless earnings can justify a higher PE often a run-up can

be just as quickly followed by a run-down.

When I sell naked puts they

are often at risk of assignment for 30 to 60 days. A range

bound stock though, gives me some idea as to what the future

could hold and what the high and low areas of the stock

could be. While its a judgment call as to where the stock

might go, I have some "crystal ball" through the Bollinger

bands. So when the stock moves to the lower bollinger I can

sell my puts and when it moves up I can buy them back.

However, if I am wrong and the stock pulls back too far, and

I get assigned before I actually wanted the shares, at least

I am in a stock that has met all my parameters, including

dividend, reasonable PE, large cap, solid earnings,

increasing dividend.

Any investor

could take this same concept and apply it to stocks they

follow. The trick is having faith in the stock and in the

technical analysis they do in order to have comfort in the

price strikes they choose. |