I hope you find the information,

concepts, ideas and strategies on my site of value. If you would like to assist me with

the maintenance costs, and time spent keeping my site updated, I

have set up a Paypal account for those who would like to donate.

Thank you in advance. Remember, nothing on my site is financial

advice or recommendations. Investing is risky and losses can be

large. Trade at your own risk.

Read The Disclaimer

I set up a Yahoo forum for those interested in discussing selling stock

options for income including covered

calls, selling naked puts, spreads and other option and stock strategies.

JOIN HERE

March 31

2011 / Strategy Article - Selling Stock Options

Selling Puts For Profit And Avoiding Assignment

The 13 Rules I Use

Introduction

Selling stock options for

income is a favorite strategy and selling puts is my first

choice. Naked puts is also often referred

to as selling cash secured puts as the investor will often

have the cash sitting aside to cover the stock price in the

event that the naked puts are assigned. In my mind there is

no difference between referring to them as naked puts or

cash secured puts. It's all semantics. In this article I

will refer to strategy as selling naked puts. Once a put has

been sold, the investor is obligated to be assigned shares

at the strike price they have sold the put for. Basically

they do not own the stock yet, but have indicated their

willingness to own the stock at the strike price they have

sold the naked put at.

What Is Meant When An Investor Sells

A Stock Option Termed Selling

Puts

To explain perhaps more

clearly, I will use Toronto Dominion Bank which I refer to

as TD BANK (symbol on TSX and NY is TD) as an example. Today

(March 31 2011) the stock is trading around $86.00. If I

sell a put at the $84.00 strike which expires in MAY I am indicating

that I am willing to own shares of TD Bank at $84.00 ANYTIME

in MAY. Selling this put is a legal obligation to be

assigned shares AT ANY TIME up until the third Friday of the

month of May.

Therefore whether I have the cash readily available or

whether I am going to borrow the money (often called margin)

to pay for those shares, I am legally bound to own shares at

that price. Therefore since I do not yet own the shares I am

NAKED. The term "naked" means that I have exposed myself to

owning shares that I do not yet actually have in my

possession. In other words I am naked the shares as I do not

yet own them. The only way out of this legal obligation

prior to options expiring in MAY, is to buy back the naked

puts which effectively ends the obligation. Of course, if

the stock ends up higher than the naked put strike sold,

then the seller of the naked put retains all the premium

earned.

Pitfalls Of Selling Stock Options Like Naked Puts

Often selling

naked puts is a trade of small amounts which over months of

constantly selling naked puts against stocks can result in

reasonable monthly income. However there is nothing worse

than selling a naked put for .50 cents and ending up buying

it back for $1.50. Repeated losses like that can wipe out

months of many small gains. In other words a large loss will

wipe out many small gains.

Many investors

look at naked puts as "free money", which is not correct.

There is nothing free about selling naked puts. As soon as

the put is sold I can easily be assigned shares; watch the

naked put triple in cost to close if the stock collapses; or

end up running repair strategies for months or even years in

an effort to regain lost capital. Selling naked puts does

not result in "free money".

As well, many

investors quote statistics that 80% of options expire out of

the money every month. This is definitely true but only

because there are literally hundreds of options that are so

far out of the money that the chance of them ever being in

the money is limited to a black swan type event. The real

question is how many NEAR or AT THE MONEY options expire out

of the money. These are the options I am selling because

these are the options that pay enough premium to warrant

having my capital at risk. In this event it is closer to

50/50, so the notion that just by placing a NEAR out of the

money naked put trade will be successful is far from

guaranteed.

Further, selling naked puts leaves the seller open to large

losses should the stock plummet. For example if I had held

naked puts on AIG in the fall of 2008, the losses would have

been catastrophic. In many cases a naked put seller will do

spreads instead in order to protect against such a potential

disaster. This is done by selling the higher strike naked

put and buying a lower strike naked put. Therefore if a

stock like AIG had a spread on it, the loss would have been

limited to the difference between the strike sold and the

strike bought.

Many investors

sell far more naked puts than they can actually handle.

Selling too many naked puts is a recipe for disaster. When i

first starting selling options, years ago, I was caught up

in what I felt were excellent naked put positions. Every so

many days I would continue to sell more naked puts and often

on the same stock as the stock continued to rise in value.

Literally dozens of these trades worked out and I made such

great returns that I dreamed of quitting my job and doing

nothing but trade options. I thought what a genius I was.

Then suddenly I hit a streak where a number of trades did

not work out. A stock would pull back and I would wait,

confident in my technical charts and my belief that I was

indeed a genius. I remember one trade in particular when I

was first starting out that I kept selling naked puts as the

stock went up AND as the stock came down. In the end my loss

was more than $32,000 on just one trade alone. This wiped

out 8 months of gains and made me realize that not only was

I not the options genius I had thought I was, but that it is

not options that are risky, it is the investor who blindly

accepts the risk.

My Strategy For Selling Puts On Stocks

and Avoiding Assignment

Nonetheless there are often

many trades that appear where the premiums are so compelling

that I would sell naked puts even if I had no intention of

ever owning the stock. After all, selling options is all

about gathering income. But these compelling trades still

had a lot of risk of assignment.

I therefore turned to paper

trading and spent several years establishing a strategy for

myself that could be reasonably successful. Over those years

I developed guidelines or rules for myself which I found if

I adhered to I had a much better chance of a successful

option trade.

It is important to always

remember that each investor has their own personal goals and

levels of risk. I learned through many trades that I could

attain far more profitable trades when I sold naked puts on

stocks that I would like to own. This was because when a

stock I WANTED to own fell placing my naked put into a loss

situation, I would not close those puts but be content to

"ride out" the whipsawing of the stock. However when selling

naked puts on stocks I do not ever want to own, I would

close on any downturn in order to either lock in my profit

to that point or to avoid what could be a larger loss.

Throughout the years of perfecting my strategy I found that

FOUR THINGS ALWAYS STOOD OUT.

It is important to LOCK IN

THE PROFIT by buying back my puts when the profit was

there.

Stocks, no matter how much technical

analysis I did, still could surprise to the downside and

quickly.

It is

important to avoid assignment. This is because, as per

this article, I

am selling naked puts on stocks I do not care to own and

often those stocks can collapse very quickly and leave

me holding shares at a strike price that can take months

to regain my lost capital.

Last was to be realistic in my expectations. Earning 3

and 4 percent every month was just not realistic. Some

months wiped out other months. However I did find that

1% a month was realistic and I developed strategies to

that end.

My Rules For Selling Naked Puts and Avoiding

Assignment I

found that

when I sold naked puts with no

intention of owning the underlying stock, these became my

rules or guidelines. Remember nothing on my site is

financial advice or recommendations. Trade at your own risk.

My site is for discussion and presentation of my ideas only.

Read my full Terms Of Use.

1) Sell

only on stocks that are in an uptrend. To check this I look

at the 10 day Simple Moving Average and compare it against

the 20 and 30 day exponential moving average.

You can read about the 10-20-30

moving averages trading strategy here. Below is a good

example from TD Bank in March 2011.This stock has been in an

uptrend since early January 2011 and has been a consistent

naked put sell for three months.

2) Try for at least 1% from the option sell. It's important

to make at least 1% from the trade in order to justify

having my capital at risk. If I am only going to pick up

half a percent or less from the trade I have to really

consider whether it is worth making a hundred dollars if I

have a few thousand dollars at risk of assignment. I try to

use 1% as a minimum guideline.

3) Sell

one month out. I try to stay away from longer time periods.

Stocks can fluctuate a lot, even in a month. The shorter the

term to expiry, the better my chance to avoid assignment.

4) Always

sell out of the money. I don't want the stock, just the

income so there is no point in setting myself up for a

possible loss by selling at the money or in the money naked

puts, even if the stock is trending up. Below is the

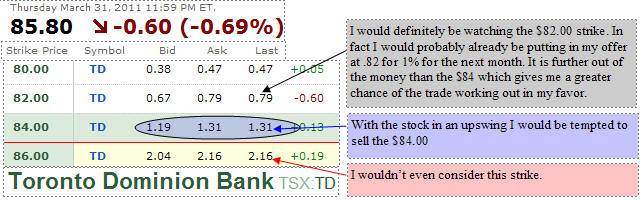

March 31 closing option trades for TD on the TSX. The $82.00

strike makes a compelling trade. It meets my guideline of a

short time period and 1% income if I can get filled at .82

cents.

5) I

always try to sell on a down day for that stock. As per the

example above, TD Bank fell more than 1/2 percent on March

31 and the puts have gone up in value. This would be a good

day for selling naked puts.

6) I am

never in a rush. I place the price I am content with and

wait for a possible fill. There are hundreds of stocks.

There is never any point in taking less than I wanted. In

the above example I would normally place my ask at .82 cents

early in the day and wait for a possible fill. That's 1%. If

this trade doesn't work out I am always watching other

stocks. There will be another trade so no point in chasing

any trade.

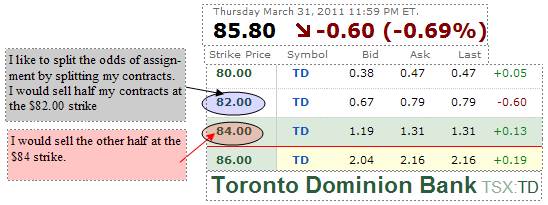

7) I like

to spread out my contracts between two strikes. For example,

as per the chart below if I was going to sell 8 naked puts I

would sell 4 at the $82 strike and 4 at the $84. That way if

the trade turns, and I have to close the 84, many times the

82 will still end up out of the money. Also sometimes the

$82 may not give me the full 1%, but the $84 is giving me

more than 1%. Added together, if both of these naked puts

work out I am making more than 1% overall. This splitting

can assist the overall trade results.

8) Treat selling puts as a business. In business it is

never ALL or NOTHING. In a business I set goals and

objectives. In a business I set up strategies to reach those

goals and objectives. By setting my selling of naked puts as

a business, I set my goal firmly at 1% per month and then

determine how to make that return but spread the risk over

my total capital. For example if I have $30,000 to invest

then I need to make $300.00 in the month.

To reach my goal of $300.00 I divide up my capital among

various naked put trades. For example, in the chart below I

can sell VISA for 1.59 which nets a return of 2.27%. If the

chart on VISA (10-20-30 averages as per rule#1) shows an

uptrend, then I sell the naked puts. I then look at another

stock NOT VISA where I can sell farther out of the money,

for example Microsoft, and sell the 22.50 for just .57%

return. But by combining the two trades I aim to net a total

return of 1%. In other words if I have $30,000.00 and I want

to earn 1% this month I need to earn $300.00. If I can

sell 2 VISA $70 strike Naked Puts for $1.59 that equals =

$318.00. I have made my quota for the month. Two Visa puts

at $70.00 equals just $14,000.00 invested. This leaves me

with 16,000 I can still place in trades. I can therefore

sell 7 naked puts on Microsoft, farther out of the money at

22.50 for .14 cents for $98.00. My return for the month if

both trades work out is $416.00 or 1.3%. 1.3% X 12

months = 15.6% annually. On $30,000 a return of 15.6% is

$4680.00. Take this concept one step further and consider if

I have $90,000 to use for naked puts and I can realize the

same returns as above. This would earn $14,040.00. Now

consider $200,000 invested using this strategy. This returns

$31,200.00 annually.

Being realistic in my returns and treating my naked put

selling like a business has assisted me in being far more

consistent, setting goals and establishing strategies. I

truly do not care about one trade earning 5% one month and

then the next month having a lot of trades losing 2%. I want

a steady 1% a month return. By splitting my capital among a

variety of trades I can risk a smaller amount at higher

strikes on more volatile stocks and the bulk of my capital

is being used at farther out of the money strikes on less

volatile stocks. (more on volatility in rule number 12

below). I would never do this strategy on the same stock. By

splitting up among different stocks the likelihood of a

total failure is reduced. Should VISA fall and I have to

close the trade, I can possibly still make the trade for

Microsoft work out.

Taking this strategy 1 step further, whenever I have a month

that works out and the capital is not needed for income, I

roll that earned income back into my next month's trade.

Basically I am compounding my capital. For example if in

this month my 30,000 earns the above trade I will have made

$416.00. Next month then I have 30,416.00 to invest. Spread

out among the same strategy as above for the same strikes

means I would sell 2 VISA $70 strikes for 318.00 and then

look around further. With Intel at $20.00 I might consider

selling 8 contracts of the $18 strike for .20 cents

which earns $160.00. If both trades work out my earnings for

this month would be $478.00. I then compound that into the

next month making my available capital $30,894.00. By

continuing this over months and years I found that instead

of 12% a year I was continually earning 15% or better every

year and lowering my chance of having a month with a

complete wipe out as often if the stocks with better

premiums such as VISA turned and I did not make the full

amount but had to close early, my lower strikes in most

cases worked out.

The higher place strike such as the VISA $70 are in smaller

contract sizes. The lower strikes such as Intel at $18.00 or

Microsoft at $22.50 are holding the bulk of my capital with

less risk of assignment than VISA at $70. With this strategy

I am diversifying my trades and reducing my risk of

assignment on the larger portion of my capital. Recall the

statistic that 80% of options expire out of the money, but

that near or at the money are 50/50, I am basically playing

the odds by having fewer contracts exposed at closer to At

or Near The Money and more naked puts sold further out of

the money on different stocks.

9) Learn

How To Close and Take The Emotion and Guesswork Out. This

was an important step for me. I always found it difficult to

close early or even knowing when to close. I experimented

with many different percentages. Finally I came up with this

method which worked for me.

On the

high naked put strikes or the At The Money naked puts I had

sold, I take the amount I sold the put for and calculate 75%

and I put in an offer to buy back my naked puts at that

price good until 2 weeks prior to expiry. I put this offer

in immediately after I have sold the naked puts.

For

example, if I sold the VISA strike for $1.59 I immediately

put in my offer to buy back the naked puts at .40 cents.

This takes away all the guess work and emotion from the

trade. It forces me to close the trade and lock in my

profit. If I close early, then I look elsewhere.

After two

weeks if the trade is working in my favor I reduce my offer

to buy by 10% per day. For the above that would mean .36

cents on the first day and .33 cents on the second day, etc.

If the trade still is in my favor by the week of expiry, I

will only close for pennies up until Wednesday. By the

Wednesday before expiry I will not close at all barring an

unforeseen event.

For my further out of the money naked put strikes I

immediately set them up to close for 80% of their value. In

the case of Intel at .20 cents that would mean I am willing

to close the trade for .04 cents anytime up to the beginning

of the second week before expiry. After that I do not close

unless something unforeseen should occur.

10) If the

trade turns against me, but I have a profit, I close

immediately. I always know that should the trade turn,

there is a very good chance I will be able to sell the same

naked puts or even lower within the same stock within a few

days or a week. There is always an opportunity to make

another profit. Losses can mount quickly with options. I

often found that an option that I could have closed for .08

cents today is .50 cents to buy back, just two days later. I

found that often I was closing too late on downturns and my

profit was almost gone by the time commissions were taken

into account.

11) If I

do not have a profit, I close the trade as soon as it

is a 20% loss. For example, if I sold VISA $70.00

strike for $1.59 and the trade went the wrong way right from

the start, I would put in my offer to close at $1.90. I

found overall that 20% was a reasonable loss to take and it

did not overall affect my entire year's earnings.

On the farther out of the money naked puts I use 25% as my

loss buy back point, which seemed for most of my trade to

afford me enough room that if a stock pulled back and then

turned and continued higher, I did not end up buying back

the puts, only to find out a day or two later than it was

the wrong trade to have made.

By following rules 9, 10 and 11, I found that I was more

consistent in earning income every month. Some months all

the trades worked out and in other months only the furthest

out of naked puts did, but the returns on an annual basis

kept growing and the losses were minimized.

12) The

less volatility in the stock the better. Lower

volatility often means a stock has not had large price

swings. However lower volatility also means smaller premiums

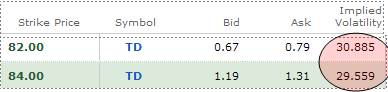

so it is a trade off. For example in the chart below for the

same strikes for Toronto Dominion Bank, the volatility is

not overly high, but then the premiums are not as great.

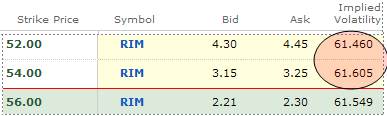

In this chart I

can see that RIM's volatility is twice that of TD, but the

option premiums reflect this as well.

Higher volatility though meant more often I was either

buying to close my puts early; having to close early because

of a pull back; had more trades with higher losses;

whipsawing of the stock.

Lower volatility while it presents lower option premiums

also provided me with far more trades that were overall

profitable. Being realistic and setting the goal of 1% a

month made for much better stock selections when ultimately

I did not want to own any stock.

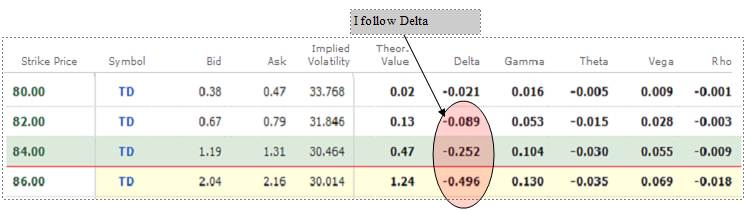

13) I Watch Delta. Finally although there are lots of

investors who disagree with me, I found that the greeks as a

whole did not really assist in my stock selections and put

strike selections. However among the greeks I always look at

DELTA. Please don't bother to write me about the importance

of the Greeks. I do get it. I understand what Gamma, Theta,

etc is all about and why some people love them and wouldn't

even trade without them. But honestly, stocks move around a

lot more than investors realize. Delta in its simplest of

form is a quick way to determine what are your "odds" of the

stock reaching your strike point before the expiration of

those month's options. In my TD example you can see that the

odds of the $82 strike being assigned are below 10%. The $84

strike are 25% or 1 in 4. The greeks change all day long and

every day, so honestly I prefer the 10-20-30 to really

figure out if a stock is in an uptrend and my chance of

assignment are low. But at least Delta helps a bit.

Summary

Those are the 13 guidelines I follow when selling puts

against stock I do not want to ever own. Remember that

losses can be large on any investment or investment

strategy. These are the rules or guidelines which I

developed after paper trading for many years. I suggest every investor interested in selling puts,

paper trade first and establish their own set of guidelines

or

rules. Every investor has their own risk level and investing

goals. It is important to learn what they are before

entering into any investment.