I hope you find the information,

concepts, ideas and strategies on my site of value. If you would like to assist me with

the maintenance costs, and time spent keeping my site updated, I

have set up a Paypal account for those who would like to donate.

Thank you in advance. Remember, nothing on my site is financial

advice or recommendations. Investing is risky and losses can be

large. Trade at your own risk.

Read The Disclaimer

By using this site,

you agree to be bound by its terms of use.

The full terms of

use can be read here.

If you do not agree to the terms of use, do not access or use

this site.

Nothing presented is financial advice, trading advice or

recommendations. Everything presented is the author's ideas

only. The author accepts no liability for its use including

errors and omissions. You alone are solely responsible for your

own investing and trading. There are considerable risks involved

in implementing any investment strategies and losses can be

large. Trade at your own risk.

Feb 11 2011 / Stocks - NUE, JNJ

Market

Trend: Still Up - But Watch For June

Market

Direction Article

The market appears caught in a bull mood but will it be

able to hold on when the Fed stop's the printing press?

With so many analysts complaining about "Government"

involvement in the market you would think that this is

the only time the government has been involved. Just to

set the record straight - the market has always been

manipulated by government interference. The Fed money

press has assisted this market from the height of the

credit crisis until now. It also went to work after

9/11, in 1995, 1987, 1977, 1975,etc etc. Governments

worldwide have always had their fingers in the market.

The better question I believe is what will happen when

the Fed steps back from the market to see if it can hold

its own ground. On Jan 20 I wrote that my strategy for

the year would be the "Cautious Bull"

You can read it

here. Here is why I think my strategy may serve me

well this year and perhaps into 2012.

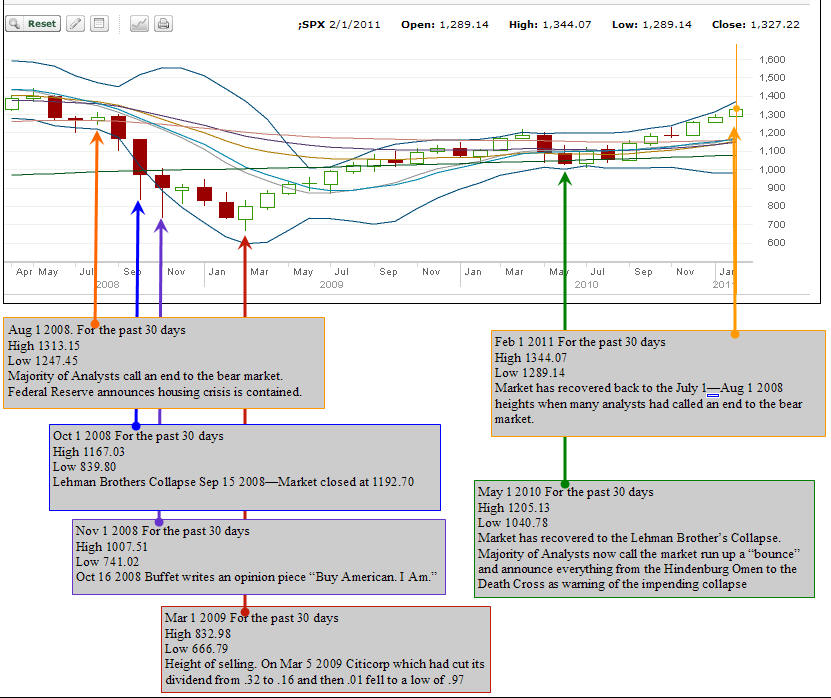

To understand I have to go back to the summer of 2008.

The chart below highlights the main events over the past

2 and a half years. In August 2008 many analysts called

an end to the bear market. Indeed the Federal Reserve

tried to reassure markets by announcing that the housing

crisis was contained. At this point there was no mention

of a credit crisis or European Debt problem. 6 weeks

later on Sep 15 Lehman Brother's collapsed, putting in

place the collapse of markets worldwide. By Oct 2008

when Warren Buffet released his "Buy American. I Am"

opinion piece, the market was fallen to 741.02 and a few

months later in Feb to Mar 2009 the S&P reached 666.79

losing almost 50% from the Lehman Collapse.

Many analysts called for the S&P to probably reach 400 before

the end would be in sight. Instead by May 1 2010 the market had

recovered to just before the Lehman Brother's Collapse. This was the

easy money. Selling naked puts and holding stock and selling out of

the money covered calls provided spectacular returns. Now at a high

of 1205, again Analysts weighed in with everything from Hindenburg

Omens to Death Crosses to tell investors to get out.

Just a few days ago the S&P had recovered to the July to

August 2008 heights. In my opinion the easy part of this rally is

over. Certainly I believe another 10% to 15% could be achieved but

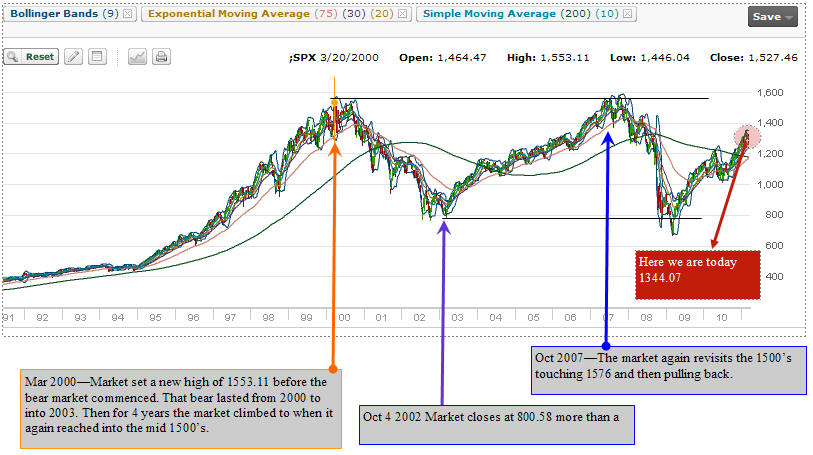

let's look at the below chart. In October 2007 the S&P hit a high of

1576.09 before pulling back. For most of 2008 before the collapse in

September, the market was range bound between 1300 to 1450. I

believe the market today at 1344.07 marks a return to pre-collapse

level and back to the range bound period BEFORE the collapse of fall

2008. Simply put, we are just back to where we were when the market

was stuck waiting for higher earnings and "better times" to push the

market beyond the Oct 2007 high. Can we get there? I have my doubts.

Let's move to the next chart to see why.

Below you can see the last chart. It shows the past

decade or so on the S&P. We have a very classic looking market. Two

all time highs and then selling and a new bear market. My prediction

is we may reach into the low to mid 1400's twice this year and then

a sideways to move down going into 2012. Below the chart are my

reasons why:

The move up

from 1995 to the high in 2000 was a growth period

for the economies of the world in general. True to

economic growth, by the turn of the decade in 2000

the market had reached exuberant status and

therefore pushed it into the mid 1500's.

This was a

period of true growth in the economy and in

corporations in general within the market (aside

from the dot.com bubble which is another story

altogether). Annually stocks made gains based on

those earnings.

After 9/11

the Federal Reserve eased monetary policy and the

economy in October 2002, turned and on low interest

rates the economy picked up steam, in particular

housing. Financial institutions expanded beyond

their normal role as lenders and profits (whether

actual or not) seemed to support valuations. With

this easy money came a lot of growth within

corporations.

TODAY:

Debt loads

are truly staggering both personal, state, national.

These debt

loads are not limited to the United States but are

world wide.

The housing

market has yet to recover.

European

nations like Greece and Ireland could very possibly

default on their long term debts.

Unemployment is higher than normal and remains

stubbornly high.

The Federal

Reserve has held interest rates at or near zero for

more than two years.

The Federal

Reserve has pumped hundreds of billions into the

market and economy.

POSITIVE

TRENDS:

On the

positive front many corporations have rebounded in

earnings.

Many

corporations have refinanced at ultra low levels.

Many of

these same corporations have refinanced for extended

periods, some as much as 100 years but many for 30

years at very low interest rates.

The Federal

Reserve has held interest rates at or near zero for

more than two years.

The Federal

Reserve is pumping in hundreds of billions of

dollars, supporting stocks and riskier assets.

Based on the

above, it is true that the market could continue to

climb (not straight up) and even surpass 1500 on the

S&P, but a lot of this could again be caused by the very

real concern among investors that there is very little

place to "park" their capital and earn more than 1%.

This brings many of them back into risky assets like

stocks, which I believe is part of the Federal Reserve's

plan. The collapse of stocks in 2008 and again in 2002

wiped out a lot of investors including seasoned ones.

Pension plans which are heavily invested in risky assets

simply because of returns on investments during this

period of very low interest rates, saw large losses in

both downturns. I believe the Federal Reserve is

concerned about the retirement benefits of millions of

Americans which are tied directly to risky assets. As

well this period of very low interest rates would also

seem to suggest that there is a real possibility of

deflation. Last year there was a lot of talk about

deflation, but this year (2011) that talk seems to have

abated. Personally I believe deflation remains the

greater threat. As well the problems of excessive debt

both personal and by countries worldwide are a real

issue that still could derail the economy at some point.

The Federal Reserve has indicated that by June they

expect to end Quantitative Easing - The Sequel. That

could be a tough month for investors.

Therefore based

on the above, I believe it is important to remain

cautious as the market has reclaimed much of what was

lost in the Oct 08 to Mar 09 downturn. The best I hope

for is a sideways market, but I believe that the first

sign of European sovereign debt issues or climbing oil

prices could easily turn the market around. I do not

though believe the market can collapse back to the March

lows over the next few months, as earnings have remained

strong for corporations, which seems to be the only real

bright spot in the economy. I am staying with large cap,

blue chip stocks and you can read the rest of my

strategy in the other article "The

Cautious Bull"